Evaluating Enterprise Cloud Stocks Through A Thematic Growth Lens

Despite generally meeting and raising revenue and customer growth projections in the most recent quarter ending June 30, 2019, many enterprise cloud computing stocks have been hit with a severe drawdown in September as investment flows shifted from growth to value. A key question is whether this rapid change in investor preference is an inflection point in terms of a willingness to support high multiples, or could it mean a brief period of consolidation that will lead to continued growth and stock gains when investors’ desire for growth reignites buying interest?

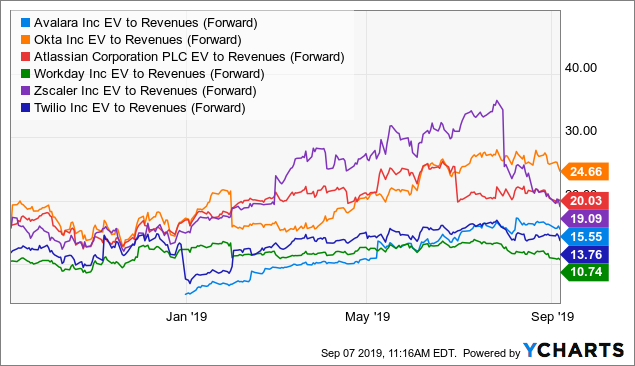

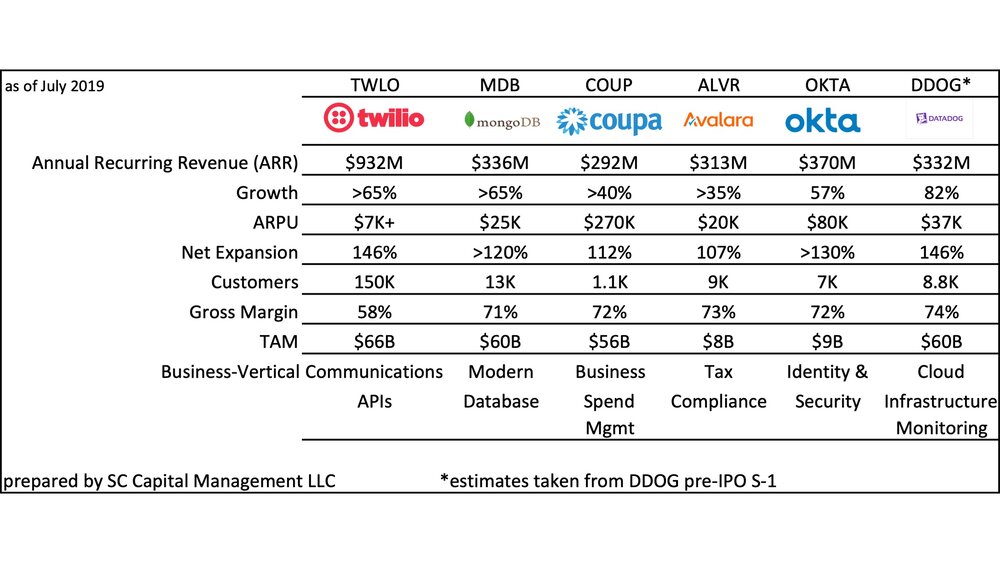

Selected enterprise cloud computing stocks

The frothy enterprise cloud computing sector of the tech industry has earned high valuations (on EV/sales basis) based on superlative growth metrics, high gross margins, recurring-revenue business models and a customer base of enterprises that are in the sweet spot of digital transformation. Enterprise software spending is projected to grow 8.5% from 2018 to 2019, and another 8.2% in 2020, for a total of $466 billion, according to Gartner. There is no higher quality growth in the market today than this sector which is part of the much larger $3.8 billion IT industry. Cyclical vulnerability is always a real risk factor for top-line growth stories. Yet the combination of higher forward revenue guidance and recent stock price declines makes the frame of reference for decision making more than the simple arithmetic of lower multiples. Investors looking for entry points or justification to re-balance portfolios can benefit from a thematic lens for decision making in this sector – in addition other traditional metrics that relate to financial performance and risk.

Long-term themes differ from short-term trends, and so should the methods of evaluation. Themes have a narrative component and work over many years. For example, there is limited insight into the future potential of these high-growth companies through the structured confines of discounted cash flow (DCF) modeling. Projecting annual changes to working capital and terminal growth rates ten years out can bury so many layered assumptions so as to make false precision as pernicious a behavioral bias as the ones that infest thematic investing (didactic aesthetics).

Traditional accounting methods – based on historical data and equipment-based capex spending – can distort the picture of an enterprise cloud computing platform designed for the labeling, ingestion, cleaning, visualization, and analysis of data in ways never before contemplated. Stated a different way, the yoke of linear, mechanical thinking in the face of innovation that is geometric in scale can fatally diminish the opportunity set of potential outcomes for these opportunities, all in the service of adhering to a standard that dictates a very simple bounded optimism: the past is indicative of the future and all trends mean revert.

Amazon

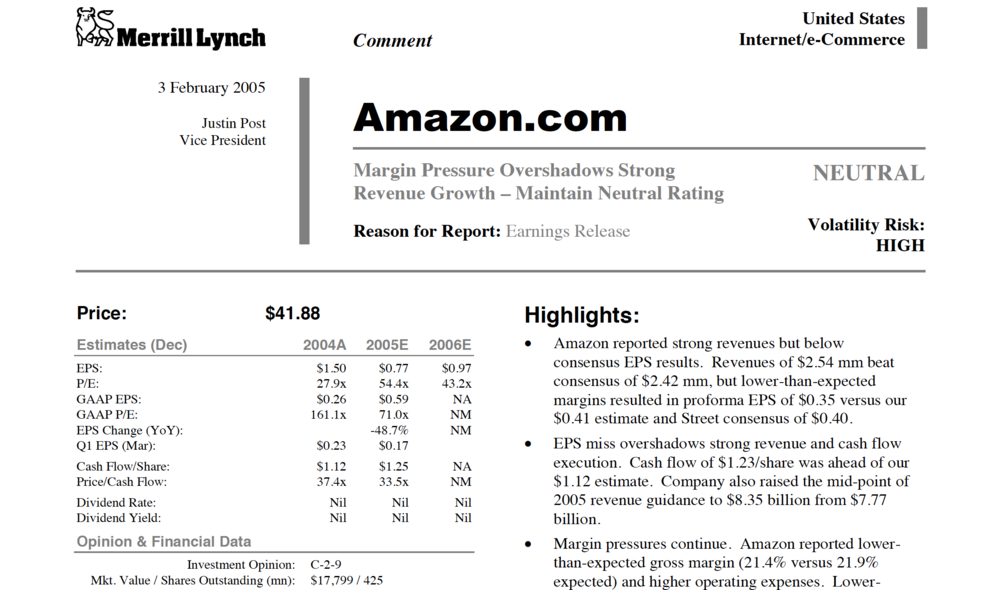

Looking back at Amazon during its formative years illustrates why investors should devote time and energy to developing themes to evaluate growth industries and companies for potential investment. In 2007, the wildest Amazon bull estimated that 13 years from then (in 2020) Amazon was going to produce nearly $40 billion of revenues. Today, 12 years later, the average sell-side analyst thinks Amazon will do over $320 billion of revenues in 2020. Amazon’s reward to investors over this period is about 50x. Over the last 15 years or so, there were two major themes, (consumer) e-commerce and (enterprise) cloud computing, that provided multiple entry points for a winning investment in Amazon.

Today’s Thematic Lens

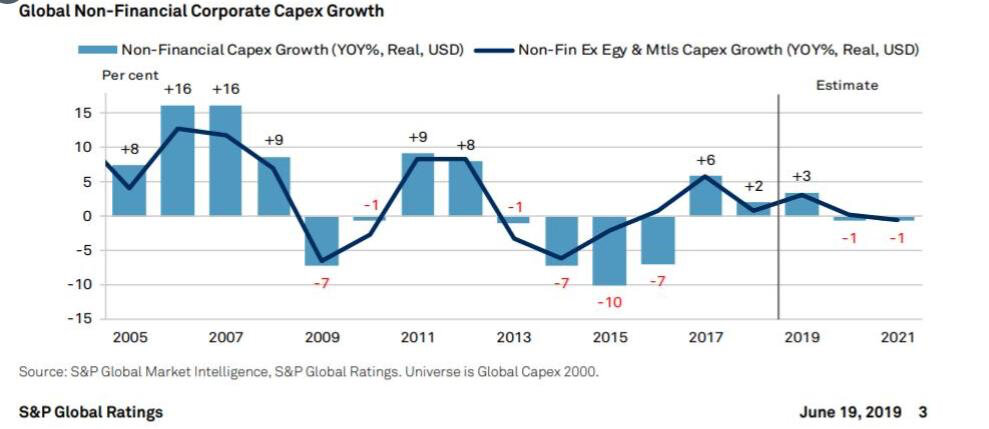

There are several factors at work today that suggest using a thematic approach can help clarify the future potential of enterprise cloud computing stocks in ways that escape the simple accounting treatments of historical financial performance. The first is the generational shift away from traditional capital expenditures (“capex”) spending and towards operations spending (“opex”). It used to be that capex supported infrastructure capabilities. Today value creation is happening through opex. This shift makes sense for an economy leaning towards knowledge and service workers and away from factory workers. GAAP accounting was designed to quantify corporate investments in future growth along with a method to expense the cost over the many periods that make up the assets’ useful life. What is obvious now is that both R&D and capex spending have different implications for a software company compared to a traditional industrial company.

Hosting code on servers that is variably priced based on product demand means the balance sheet for many of the cloud-based companies contains relatively few items: cash, receivables (that are largely irrelevant when the product is often pre-paid monthly), and office leases. In one case, Atlassian, which makes software for teams to work together more efficiently, grew revenues to nearly $2 billion with relative little marketing and advertising. At the time of their IPO in 2015, only 19% of their revenue was spent on sales and marketing, a fraction of the spend compared to other companies of their size and growth, and it had no sales employees. For these companies, growth is achieved through geometric scaling via word-of-mouth and relatively low reinvestment. Products in this sector are optimized for performance in real time instead of being machined out of metal and then used with little modification over many years. These types of efficiencies were never contemplated by GAAP accountants who could only imagine the symmetry of more revenue resulting from the addition of more PP&E (property, plant and equipment). What is replacing PP&E is intangibles like information, IP, code and branding. In high-growth environments, intangibles produce asymmetrical outcomes and potentially huge investing rewards. Even the word “intangible” sounds like an accounting step-child.

Writing code to create a product with monthly recurring revenues and no marginal cost of production is a fantastical method of drilling leverage into a business model. The often-cited reason Amazon was considered to be a risky or bad investment was because it was not like Borders and Barnes & Noble – it’s quality was asymmetrical to the norm. Amazon’s spending ramp for its cloud computing business started in 2006 with costs that reduced margins, much to the consternation of investors. Some investors, especially those who adhere to value investing principles, wrote off Amazon for having a P/E ratio that was at times greater than 100.

Conflating R&D with innovation is another nuance to the accounting problem. For example, in 2006, Ford’s R&D spending ($8 billion) was the second highest in the world (after Pfizer) and even higher than Microsoft and Johnson & Johnson. By comparison, Amazon launched Amazon Elastic Compute Cloud (EC2) in the same year. It pioneered the field of “infrastructure-as-a-service” (IaaS) by presenting a virtual computing environment allowing customers to use web interfaces to requisition servers remotely. Amazon’s 2016 capex spending was $175 million, or about 2% of revenue, and its R&D spending was a tiny of fraction of Ford’s at $662 million. And estimates of Amazon’s cloud computing revenues that year suggest a figure less than $50 million. Over this period, from 2006 to today, Amazon’s 50x return compares to Ford’s return of approximately zero.

The second thematic issue is the “re-platforming” of the enterprise across every industry and geography on the globe. The impact is nothing short of leveraging the computing base of whole industries to make workers more efficient and to squeeze cost and friction out of entire business models using variable, subscription software hosted in the cloud. The roots of this massive theme point directly to Amazon’s launch of its IaaS business in 2006. There were earlier signs of the epic changes that would lead to the launch of a generation of fast-growing cloud computing companies, many of which were built with Amazon’s cloud business, now called AWS. Om Malik’s insight about the emergence of these faster, cheaper software companies highlighted one of the greatest computing insights of this generation. In his 2003 article, “The Rise of the Instant Company,” Malik says, “Kolluri and Neoteris are pioneers in a new era in the tech world. Call it the age of the instant company. Commoditization – the process by which technology products become standardized and their prices are shoved relentlessly downward – has now driven the cost of the building blocks of tech so low that hardware expense has been all but eliminated from the equation of creating new products.”

Opex Re-Platforming

Opex re-platforming means leveraging an enterprise’s most productive employees to perform even better. It also means freeing up the least productive employees to focus less on the drudgery of repetitive processes. By pushing scalable business logic into the places least-resistant to innovation, efficiencies multiply leaving competitors no choice but to innovate. There is no need for meaningful capex spending. The economics of digital transformation has spread to almost every function and vertical of the enterprise including database, tax compliance, cost productivity & procurement, communications, human resources, customer acquisition, biology and human physiology.

Achieving cost efficiency can be infectious to competitors and internal teams. The teams implementing cost efficiency initiatives are converted from being a cost to being a catalyst for earnings. In the finance function, for instance, FedEx automates tax, payroll, credit card reconciliations, treasury and other finance processes with robotic process automation (RPA) in the global shared services organization. Fossil Group uses RPA to automate the monthly financial close process. RPA companies are the fastest growing part of the cloud computing sector with sustained annual growth rates above 60%.

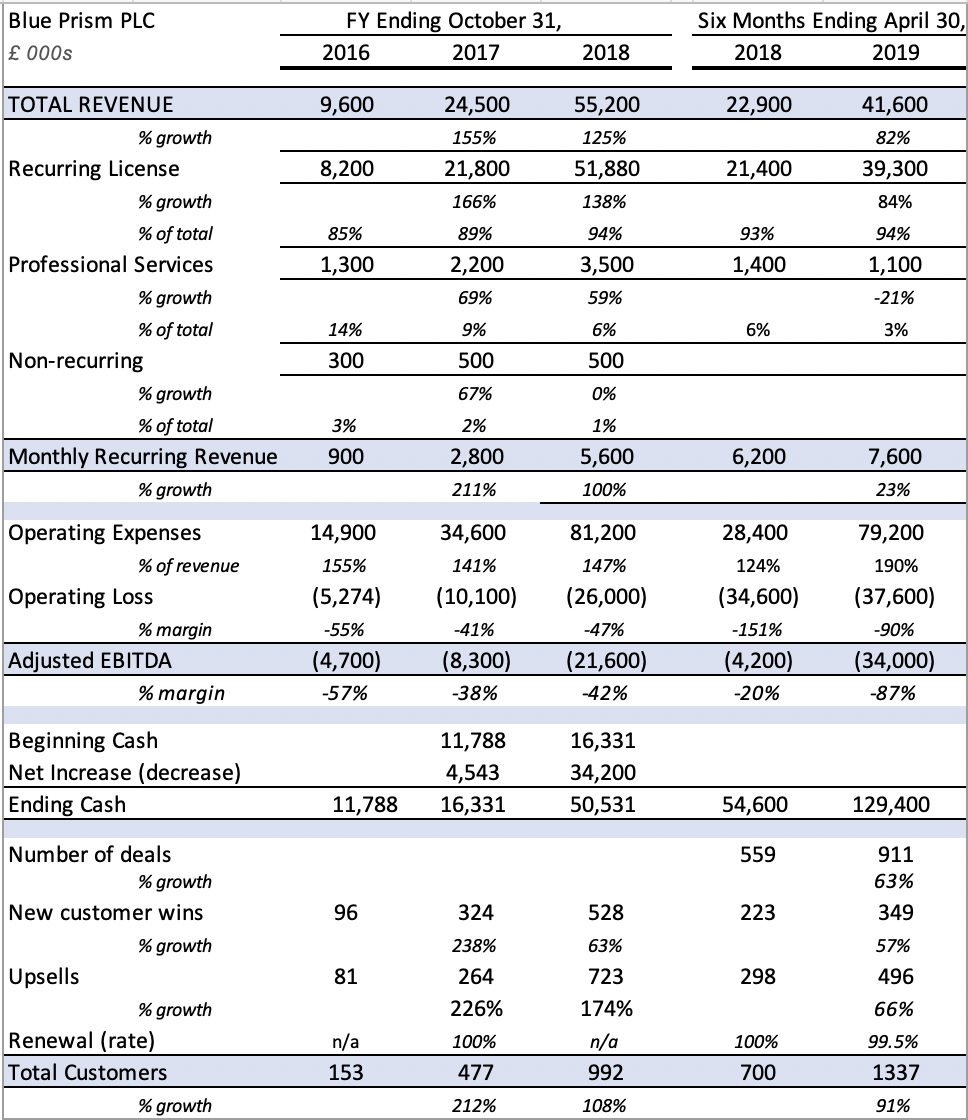

Example: Blue Prism

Blue Prism PLC (“BP”) is among three leaders in an emerging RPA industry that, along with other more mature SaaS/cloud enterprise software firms, is pioneering digital robotic innovation through automation and the surfacing of new data sets that were not available just five years ago. These new data sets resist mean reversion because the discoveries between data and actions were previously too quanderous for humans to perceive or were simply impossible to discern and diffuse. Embedded inside this niche industry and company is the full potential for AI to draw lessons from its own experience – unlike traditional software that can only extend human actions (deterministic) – and the fast-emerging capacity to translate basic human reasoning into business logic (probabilistic) for machines. Absorbing this new technology into organizational values and practices presents challenges, but they are fast melting away against the payback profiles for RPA deployments that can be measured in terms of months or less and the trend towards more task-oriented entry points for first-touch applications that are low-risk, high-value automations.

BP’s connected-RPA SaaS offering provides large enterprises with an intelligent digital workforce (software robots) capable of self-learning and continuous improvement, empowering users to automate billions of transactions while returning hundreds of millions of hours of work back into the business. Enhancing productivity using easy graphical user interface (GUI) forms and dashboards makes this technology accessible by business users who lack deep programming skills and would otherwise require complex application development in Python or R (ie. data scientists). This type of automation employs robots to control the triggering, orchestration, execution, and termination of manual tasks often across business operations’ system boundaries. By pairing business workers with a nimble easy-to-deploy technology, businesses keep initiatives cost-effective during periods of expansion (revenues captured) and contraction (costs saved). BP pioneered RPA, which has become the fastest growing segment of the enterprise software industry, according to Gartner.

Prepared by SC Capital Management LLC based on company reports

Narrative Conclusions

Falling in love with your narratives is perhaps the most dangerous behavioral pitfall. This is where metrics meet narrative by converting the narrative conclusions into a company’s key value drivers. Then you can develop a quantitative approach to stock selection and performance tracking and review your assumptions. A good starting point is understanding a company’s addressable market. This could mean the magnitude of the problem it is trying to solve or perhaps a new way for people or enterprises to trade or interact, expressed in dollar terms. From there, estimate the company’s potential market share to determine a revenue picture 5-10 years out. A range will do. The idea is to be approximately right rather than exactly wrong. Strong competitive advantage narratives show up as a combination or high market share and high operating margin. So growth, in terms of quantity and quality, is a vital component for success in this sector. Then there are important granular details about management, competition and the industries the company serves.

Two important factors – stock selection and position sizing – are not covered in detail in this article. Also, looking only at companies in the same industry tends to bias the sample. Again, any intensely-regarded abstraction like an investment theme has the added risk of behavioral bias. Themes are for observing and revealing, and stocks are for investing, projecting and measuring. Realized risk in your portfolio will enter through individual stock selection and position sizing.

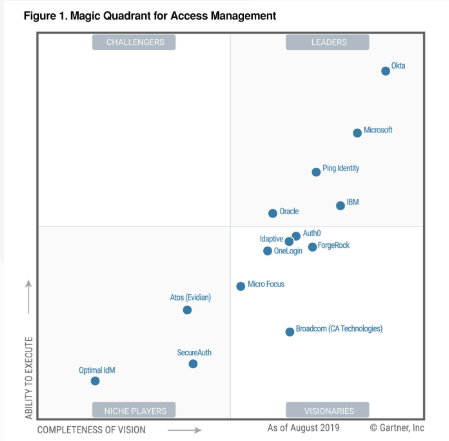

Example: Okta

Okta’s SaaS product is an enterprise-grade, identity management service, built for the cloud, and compatible with many on-premise applications. While the company competes with much larger tech companies like Microsoft, its compatibility with virtually any cloud service (not just Microsoft’s cloud) and many other software providers gives it an elasticity that is driving Okta adoption as the dominant vendor for identity management. With Okta, identity is a software layer giving employees compliant access to secure computing resources. For a company’s customer ID and tracking, Okta is intermediating as a tool for revenue generation. These two factors cause estimates of Okta’s TAM to swell when you consider how deep its tools can become integrated in the vital fabric of the Internet.

Okta reported another strong quarter on August 28th, 2019. Its revenues for the Q2-20 increased 49% to $140.5 million, beating estimates of $131 million. Net loss was $43 million, compared to $39.2 million for Q2-19. Adjusted net loss was $5.5 million, or $0.05 cents a share, compared with previous year’s loss of $16.4 million and the street’s forecast of a loss of $0.11 per share. Guidance was slightly below trend which is normal as companies grow larger. More important, the company provided an argument for improved growth quality, an important factor to consider.

By segment, subscription services revenues increased 51% to $132.5 million for the quarter. Professional services and the others segment revenues grew 19% to $8 million. Total calculated billings grew 42% to $155.8 million.

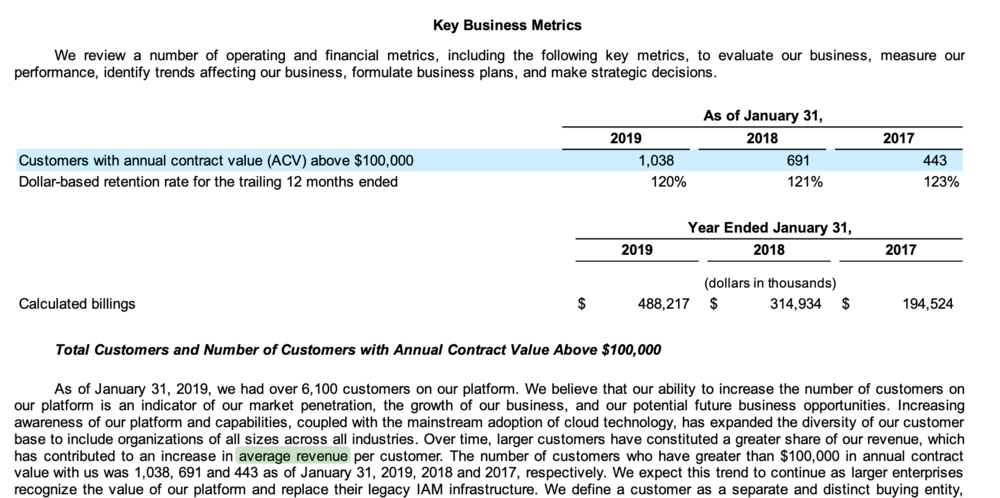

Among Okta’s key metrics, the company added 450 new customers in the quarter to end with 7,000 net customers, an increase of 36% over the year. Customers with more than $100,000 annual contract value (ACV) increased 46% to 1222.

Despite a slight slowdown in rate of growth in its guidance, Okta’s remaining performance obligations (RPO) grew by 68%, representing a backlog of $914M. The reason for the slowdown has to do with a shift in Okta’s customer base that is tilting towards bigger customers.

Okta annual report

Bigger companies have a different approach. They want stable partners and longer contracts when slecting suppliers and partners. Okta’s CEO Todd McKinnon said on the Q2 2020 earnings call that some of the contracts are signed for up to five years. RPO growth shows these contracts have a higher value in dollars, and their increased length will provide more stable growth for Okta. ACV confirms this shift to higher-value contracts as it has trended up from 443 in 2017. From Okta’s most recent conference call: “Average contract size of top 25 contracts booked in Q2 doubled compared to Q2 last year.” There is little doubt based on these indications that Okta will continue to outperform its own guidance and expand its lead in identity and security.

Finally, at 16% of revenues, international expansion is just getting started and is also consuming more expenses in the short-term.

Asymmetry

In 1997 Jeff Bezos made reference to accounting methods in Amazon’s first letter to shareholders: “When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.” Millions of analyst trained mostly in MBA business principles perform nearly identical analyses: the mechanical evaluation of high-quality, wide-moat businesses trading at a discount based on a computer-aided screen of historical financial statements. Investors can defeat the costly error of omission by developing themes to uncover asymmetries in an investing landscape designed around the symmetry of GAAP accounting.

In 1997, Jeff Raikes, a Microsoft strategist, sent a letter to Warren Buffet outlining in simple terms why Microsoft was a great investment. Raikes’ description is nothing more than a thematic overview of the opportunity. Raikes suggests it is, “probably as good as the syrup business.”

Buffet declined to invest in Microsoft. But he did eventually invest in Amazon….in 2019 (excluding his investment in Amazon bonds in 2001).

The ideas presented in this post do not constitute a recommendation to buy or sell any security.

Investors are advised to conduct their own independent research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is not indicative of future price action.

You should be aware of the risks involved in stock investing, and you use the material contained herein at your own risk. Neither SIMONSCHASE.CO nor any of its contributors are responsible for any errors or omissions which may have occurred. The analysis, ratings, and/or recommendations made on this site do not provide, imply, or otherwise constitute a guarantee of performance.

SIMONSCHASE.CO posts may contain financial reports and economic analysis that embody a unique view of trends and opportunities. Accuracy and completeness cannot be guaranteed. Investors should be aware of the risks involved in stock investments and the possibility of financial loss. It should not be assumed that future results will be profitable or will equal past performance, real, indicated or implied.

The material on this website are provided for information purpose only. SIMONSCHASE.CO does not accept liability for your use of the website. The website is provided on an “as is” and “as available” basis, without any representations, warranties or conditions of any kind.

rrnfmg

Simons Chase | Evaluating Enterprise Cloud Stocks Through A Thematic Growth Lens

[url=http://www.gu4n2lj8734lu5kj4vd3g67t93dk78k5s.org/]uxkrhvdcjq[/url]

axkrhvdcjq

xkrhvdcjq http://www.gu4n2lj8734lu5kj4vd3g67t93dk78k5s.org/

Welded Wire Mesh Fence

buy cheap Punk Rocker Choker Glasses Scarf Bandana and Tattoos Set

buy cheap Pumpkins Please Girls Orange Short Sleeve Skater Dress

Asbestos Rubber Sheets

buy cheap Pumpkins Please Burgundy Long Sleeve Girls Fall Skater Dress

Pure PTFE Sheet

Welded Mesh Fencing

Nitrile Rubber Bonded Cork Sheet

buy cheap Puppy Headband Ears & Tail, Kid or Adult Size Costume Accessories

Wire Fabric

Mica Sheet Paper

ブランドスーパーコピー

Weldmesh Fencing Panels

sork.pl

buy cheap Pumpkins & Plaid Girls Puff Sleeve Fall Dress

Wire Mesh Garden Fence

Oil-Resistance Asbestos Rubber Sheets

buy cheap GAME DAY Long Sleeve Round Neck Sweatshirt

Zoomable Headlamp

Upright Go Posture Trainer

ブランドスーパーコピー

Infrared Flashlight

Microfibre Towel Car

buy cheap GAME DAY Striped Round Neck Long Sleeve Top

http://www.tbgfrisbee.no

Silicone Hand Brace

Non-Asbestos Jointing Sheets KNXB350

Acid-Resistance Rubber Sheets

buy cheap Fuzzy and Fabulous Faux Fur Winter Jacket

buy cheap GAME DAY Round Neck Long Sleeve Sweatshirt

Non-Asbestos Jointing Sheets KNNY350

Non-Asbestos Jointing Sheets KNNY150

Non-Asbestos Jointing Sheets KNNY250

buy cheap GAME DAY Football Round Neck Long Sleeve Sweatshirt

BX Ring Joint Gasket

Expanded PTFE Sheet

FF Base Layer Shorts 'Black Grey'

Hydrolyzed Bovine Collagen

China Native Path Collagen

Expanded PTFE Sealing Tape

Wholesale Marine Fish Low Peptide

Wholesale Marine Collagen

Bovine Collagen Powder

radyoyayini.com

FF Baseball Denim Shirt 'Dark Indigo'

Natural Rubber Insertion

ブランドスーパーコピー

FF Baseball Shirt 'Black'

EPDM rubber

FF Base Layer Tank Top 'Black Grey'

FF Baseball Shorts 'Black'

buy cheap Elaine Long Curly Deluxe Brown Wig

Wholesale Acrylic Home Storage Box Organization

Europe Car Truck Bus Parts

buy cheap Elastic Waist Wide Leg Pants

ブランドスーパーコピー

Rear Wheel Drive Bearings

High Density Polyethylene Plastic Sheet Board

buy cheap Elastic Strap Pearl Embellished Sandals By Liv and Mia

Woven Sack Bag Cutting Machine

buy cheap Elastic Waist Layered Tulle Midi Skirt

mbautospa.pl

buy cheap Eggshell White Bubblegum Necklace

Shock Absorber Bearing Manufacturer

Red Color Pe Polyethylene Plastic Sheet

Polyethylene Plastic Cutting Boards

Wheel Bearing And Assessories

Customized Acrylic 9 Bay 90 Nespresso Capsule

cheap Ultra Hi-Rise Booty Shorts 2.0

cheap Ultra Hi-Rise Booty Shorts

ブランドスーパーコピー

Bubble Machine Gun

Viton rubber sheet

Water Squirter

http://www.sork.pl

Nitrile Rubber

cheap Ultra Furry Scrunchies

Medium Winding Machine for Spiral Wound Gasket

Remote Control Speed Boats

Star Wars Black Series

cheap Ultra Fluffy Bucket Hat

Neoprene Rubber

Small Winding Machine for Spiral Wound Gasket

Bubble Pop Toy

cheap Ultra Furry Pocket Scrunchies

季節の変化に合わせて楽しめる、豊かなカラーバリエーション��

FF Parley Superstar

Viton rubber sheet

Hpl Sheet

キャンプスタイル

FF Patched Panel S S Shirt 'White'

Medium Winding Machine for Spiral Wound Gasket

Neoprene Rubber

FF Parachute Gear Wool Skirt 'Grey'

Nitrile Rubber

Hpl Laminated Door

Adhesive Bra Tape

jion.co.jp

Silicone Bra

Small Winding Machine for Spiral Wound Gasket

リラックスした日々

FF Paris Saint Germain Jumpman 'Off Noir'

FF Patchwork Striped Tee 'Grey'

Adhesive Bra Tap

Body Stocking Lingerie

cheap costumes KS Emerald & Pink Shimmer Bubblegum Necklace for women under $90 online shopping with free returns

Electrical insulation drilling and tapping FR4 sheet for PCB

Sheer Babydoll

Sexy Lingerie Set

日常のおしゃれ

ブランドバッグ

Babydoll Set

where to buy bloom outfits KS Enchanted Child Floral Crown for guys under $100 clothes for every occasion

dmgs.ru

Solid PEEK Sheet Natural for engneering plastic

軽くて持ち運びが楽しい、普段使いにぴったりな一品��

where to buy Thanksgiving outfits KS Emerald & Pearl Bubblegum Necklace for guys under $100 clothes for every occasion

where to buy classy christmas KS Enchanted Girls Handmade Flower Crown female under $100 local boutiques

Excellent Thermal Stability PEEK Rod

Babydoll Set

Anti-static FR4 Epoxy Plates with Precise Processing

ファッションの動向

Factory supplying Customized Vitex PEEK Sheet and Rod

cheap easy christmas costumes KS Emerald Sparkle Shamrock Charm Bubblegum Necklace ideas male under $90 fast shipping

Best Sellers women's LOUIS VUITTON Taurillon Calfskin Patent Gelato Mini Capucines Fraise Pink price cheap casual

Prepreg Pcb

軽やかでありながら高品質、どこにでも連れて行きたくなる相棒��

http://www.xn--h1aaasnle.su

Circuit Board Small

軽量で持ち運びやすい、どんなシーンにもフィットする万能デザイン��

Pcb Capacitor

china RX Ring Joint Gasket supplier

エコ素材のカジュアルバッグ

Flange gaskets

Premium Quality small BURBERRY Grainy Calfskin Vintage Check Note Crossbody Bag Malt Brown deal Under $140 formal

RX Ring Joint Gasket

china Flange gaskets factory

Affordable Luxury backpack LOUIS VUITTON Damier Azur Saleya MM review affordable trendy

Diy Printed Circuit Board

日本スタイル

Best Deals canvas LOUIS VUITTON LOUIS VUITTON Calfskin New Wave Camera Bag Porcelain Blue new arrivals Under $100 designer-inspired

Copper Board

Affordable Luxury red CHANEL Calfskin Quilted Shopping Tote Black review Under $170 high quality

BX Ring Joint Gasket

高級感漂うアイテム選び

Best price designer bags Cheap luxury purses GUCCI Boarded Dyana Lux Calfskin Small Jackie Shoulder Bag Black Discounted designer bags Discounted bags No hidden fees

Infrared Thermal Scanner

PTFE gasket

Voltage Continuity

Cheap Louis Vuitton Men's CHANEL Plexiglass Perfume Bottle Clutch White Black For sale Under $300 Free shipping

Hunting Binoculars Telescope

Aerospace Pcb Assembly

Hi Pot Test Voltage

Discounted Chanel Women's SAINT LAURENT Grain De Poudre Matelasse Chevron Monogram Monochrome Envelope Chain Wallet Black Low price Under $200 Worldwide delivery

COMMERCIAL NEOPRENE INSERTION SHEETING – 1 PLY

Cheap Louis Vuitton Men's CHANEL Lambskin Small Entwined Chain Flap Black For sale Under $300 Free shipping

Ceramic Fiber Gasket

expanded Graphite Gaskets

sandbox.phpwebhosting.com

Graphite Gaskets

Best price designer bags Cheap luxury purses BOTTEGA VENETA Metallic Crinkled Lambskin The Pouch Oversized Clutch Oro Discounted designer bags Discounted bags No hidden fees

トレンドアイテムが揃う場所

Idler

Affordable Luxury backpack LOUIS VUITTON Damier Graphite 3D Amazone Sling Bag Black review Under $170 trendy

Oil-Resistance Asbestos Rubber Sheets

Kmf40/Kmf40/Kmf90 (KPV90) PC200-1/2/3/Kmf105

How to buy clutch LOUIS VUITTON Monogram Saumur 30 for sale Under $190 multi-functional

Asbestos Rubber Sheet with wire net strengthening

カジュアルシック

Undercarriage Track Rollers

スタイル

Undercarriage Track Rollers

Where to buy tote LOEWE Canvas Calfskin Balloon Bucket Bag Ecru Tan promo code Under $180 high quality

Affordable red GUCCI Pebbled Calfskin Large Soho Hobo Black best price Under $120 top reviews

Replica Bags gold PRADA City Calfskin Saffiano Cahier Bag Granato Black top-rated Under $130 near me

特別な日の装い

Acid-Resistance Rubber Sheets

http://www.rwopr.pl

D10 idler wheel

おしゃれ

Asbestos Rubber Sheets

Non-Asbestos Jointing Sheets

Where to Buy Affordable Clothes Athletic Footwear for Women FF Adidas Adicolour T-Shirt Better Black White Online Discounts Affordable Shoes Under $70 Delivery Options

china Automatic Winding Machine For Making Spiral Wound Gasket supplier

Buy Genuine Shoes Stylish Casual Shoes for Men FF Adidas Adicolour T-Shirt Better Bluebird Exclusive Promo Codes Cheap Shoes Under $80 Best Shipping Rates

Original Cheap Shoes Women's Running Shoes FF Adidas Adicolour Shattered Trefoil Track Top Jacket Multicolor Special Offers Under $30 Free Returns

Full Automatic Ring Bending Machine for Spiral Wound Gasket Inner and Outer Ring

Cheap Authentic Best FF Adidas Adicolour Seasonal Archive T-Shirt Wonder Beige Clearance Sale Under $80 In-Store Pickup

china Full Automatic Spiral Wound Gasket Winding Machine manufacture

china Full Automatic Spiral Wound Gasket Winding Machine supplier

足元

Spiral Wound Gasket Inner Ring Chamfering Machine

Composite Plywood Sheets

http://www.soonjung.net

Aluminum Panel Veneer

全体のバランスを考える

カジュアル

Cheap Original Clothing women's FF Adidas Adicolour T-Shirt Better Scarlet White Discounted under $100 near me

Alucobond

Aluminum Ceiling Panel Manufacturer

スタイルの確認

おしゃれの表現

Sandwich panel

60cm Drl Strips

Automotive Interior Lights

High wear-resistant MC Nylon Board

Led Devil Eyes

http://www.machinepu.com

Best price designer bags Cheap luxury purses CHANEL Metallic Calfskin Quilted Small Boy Flap Lilac Discounted designer bags Discounted bags No hidden fees

Cheap Louis Vuitton Men's CHRISTIAN DIOR Coated Canvas CD Diamond Hit The Road Vertical Wallet On Strap Grey For sale Under $300 Free shipping

Discounted Chanel Women's LOUIS VUITTON Monogram Speedy 30 Low price Under $200 Worldwide delivery

Cheap Louis Vuitton Men's CHANEL Caviar Quilted Small Rainbow Boy Flap Multicolor For sale Under $300 Free shipping

Best polishing Nylon cnc parts

1000X2000MM Black Blue Pa6 Pa66 Board

Best price designer bags Cheap luxury purses GUCCI X THE NORTH FACE Econyl Nylon Medium Backpack Black Multicolor Discounted designer bags Discounted bags No hidden fees

High Quality Dc Fan

Smoked Halo Rings

トレンド

Insulation Epoxy Glass Sheet FR4 Grade

存在感は控えめでも、確かな高級感が日常を彩ってくれる��

靴

おしゃれ

Different Color Nylon Panel

トレンド

Fiber For Pillow Filling

Spunlace Nonwoven Process

Extruder Machinery

Meltblown Nonwoven Fabric Machine

NBR

Best Sellers women's CHANEL Caviar Quilted Medium Cuba Rainbow Boy Flap Multicolor price Under $160 multi-functional

Designer-inspired men's PRADA Nappa Bomber Tote Bianco exclusive Under $150 high quality

Cold Pad Batch Desizing

Premium Quality mini LOUIS VUITTON Monogram Ellipse Sac a Dos Backpack deal Under $140 trendy

クリエイティブな発想

フェスファッション

FKM rubber

楽しい時間

Where to buy tote GUCCI Acetate Square Sunglasses GG0765SA Black promo code Under $180 high quality

SBR

school33.beluo.ru

DOUBLE JACKETED GASKETS

RUBBER GASKETS

Replica Bags gold HERMES Epsom Evelyne III PM Iris top-rated Under $130 casual

DIYアイデア

Where to Get Luxury Bags for Less women's CHANEL Caviar Quilted Large Zip Around Organizer Wallet Black for sale Under $160 with chain

Graphite Sealing Sheet

Carbonized Packing Reinforced with Nickel Wire

ブランドスーパーコピー

bottle lid

http://www.vmfl.4fan.cz

Where to Buy Designer Replicas crossbody CHRISTIAN LOUBOUTIN Patent Me Dolly 100 Sandals 39 White baguette Under $110 outlet

Pure Graphite PTFE Packing without Oil

Affordable Replica women HERMES Suede Calfskin Go Mules 41 Black suede bag Under $190 ophidia

Carbonized Fiber Packing with Graphite

Graphite Heating Member

Original Cheap red MANSUR GAVRIEL Tumbled Calfskin Small Shopping Tote Blush must-have Under $100 fast delivery

Affordable Luxury Handbags for Sale mini MCM Grained Calfskin Wallet Pink bag price Under $190 usa

big glass bottle

Asbestos Packing with PTFE Impregnation

Glass Fiber Packing with Silicone Rubber Core

engraved champagne bottle

Hey! Do you know if they make any plugins

to help with Search Engine Optimization? I’m trying to get my website to rank for some targeted keywords but I’m not seeing very good gains.

If you know of any please share. Appreciate it! You can read similar art here: Eco product

Tree Wire Power Line

Air Compressor 25 Bar

Buff Fickert Abrasive

http://www.mtcomplex.ru

Affordable men's CHANEL Lambskin Quilted Small Duma Drawstring Backpack Black for sale budget-friendly tax-free

Lux Fickert Abrasive

Cheap Authentic gold LOUIS VUITTON Empreinte Neo Alma PM Black new collection Under $160 customer reviews

Original Cheap medium SAINT LAURENT SAINT LAURENT Calfskin Y Quilted Monogram Monochrome Small Loulou Chain Satchel Black best price Under $170 fast delivery

Molded PTFE Sheet Gasket

Aaac Conductor

PTFE Skived Sheet

Affordable vintage BOTTEGA VENETA Nappa Intrecciato The Mini Pouch Black must-have Under $150 tax-free

PTFE Skived Sheets

Molded PTFE Sheet Gaskets

How to buy black CHANEL Caviar Quilted Wallet on Chain WOC Fuchsia review Under $190 free shipping

White Silicone Rubber Sheet

ブランドスーパーコピー

French Terry Hoodies

Affordable crossbody FENDI Stainless Steel Diamond Mother of Pearl Topaz Spinel 33mm Ishine Rotating Gem Quartz Watch best price eco-friendly near me

Basic style kammprofile gaskets

Sprayer Pump Paint

Humic Acid Supplier

Affordable Luxury red GUCCI Stainless Steel 35mm Grip Quartz Watch Gold review affordable top reviews

Graphite Gasket Reinforced with Metal mesh

Kammprofile gasket with integral outer ring

Designer-inspired canvas GUCCI Stainless Steel Calfskin 40mm GG2570 Quartz Watch Black exclusive Under $150 free shipping

Organic Liquid Foliar Fertilizer

http://www.retrolike.net

Affordable red ROLEX Stainless Steel 41mm Oyster Perpetual Watch Bright Black 124300 best price eco-friendly formal

Top-rated vintage ROLEX Stainless Steel 40mm Oyster Perpetual Submariner Watch Black 14060 hot sale Under $110 trendy

basic style kammprofile gaskets

Amino Acid Trace Elements

ブランドスーパーコピー

Nuclear spiral wound gasket

There is also controversy over the style of Gilkey’s death.

Buy Genuine Shoes Fall Sneakers for Men FF WMNS BELLA KAI THONG AO3622-002 Affordable Prices Cheap Shoes Under $80 Best Shipping Rates

Big Generators

email.njp.ac.th

Caramel Popcorn

Caramel Popcorn Snack Food

Original Cheap Shoes kids' FF WMNS AIR JORDAN 2 RETRO LOW FD4849-106 Limited Time Offer Under $30 Free Returns

Backup Generators

Black rubber sheet gasket

Where to Buy Affordable Clothes Men's Training Shoes FF WMNS AIR MAX 97 FD0870-100 Save on Shoes Affordable Shoes Under $70 Delivery Options

Cheap Authentic Sneakers preschool toddler FF WMNS AIR JORDAN 3 RETRO CK9246-001 Free Shipping Below $100 Nearby Shoe Stores

ブランドスーパーコピー

rubber gasket

U type PTFE envelope gasket

Fire-resistance rubber gasket

How to Buy Clothing Online Women's Running Shoes FF WMNS AIR JORDAN 6 RETRO GTX FD1643-300 Special Offers Below $50 Local Deals

Insulating rubber gasket

Gourmet Popcorn Delivery

Melamine Particle Board

best places to shop for fashion trendy men's outfits K Holo Star Mesh Halter Bodysuit Set Outfit online shopping promo trendy outfits under $40 everyday outfits for less

Yellow Film Faced Plywood

Plywood 18mm

where to buy stylish clothing men's fashion trends K Hope Had Died Mesh Dress discount promo codes outfits under $30 free shipping

Mdf Wood

Spiral wound gaskets

Graphite gaskets and seals

cheap authentic outfits stylish women's clothing K Hope Knitted High Neck Jumper Beige clearance fashion sale shoes under $60 free shipping on fashion

Medium Winding Machine for Spiral Wound Gasket

Full Automatic Spiral Wound Gasket Winding Machine

Plywood Door Designs

Automatic Winding Machine for Spiral Wound Gaskets

trendy clothing for less winter outfits for men K Holographic Sheer Dress seasonal fashion promo clearance items under $50 Fast Shipping

http://www.issasharp.net

secure online shopping seasonal fashion trends K Honeymoon Maven Shift Dress trending sale items seasonal sales under $60 Delivery Options

ブランドスーパーコピー

V Roller Bearing Factory

Buy authentic for less ugg boots sale for women Vans, Vans, Baskets ASHER DELUXE, noyer, hommes 'popular items' under $70 best e-commerce deals

Gray Hard PVC Rod Dark Gray PVC Bar

High Quality PVC Panel

How to buy cheap deals ugg boots chestnut sale Vans, Vans, Espadrille lacée WARD, floral, femmes 'top picks' under $80 trending online

Cheapest online deals ugg boots sale online 2024 Kamik, Kamik, Sandale sport LOBSTER 2, noir, garçons 'popular shopping' under $180 affordable prices

High Hardness Round Bar Grey PVC Rod

Long Roller Bearing Pricelist

How to find best discounts ugg genuine classic short Kamik, Kamik, Sandale sport LOBSTER 2, marine lime, garçons 'fashion sale' under $50 hot items

ブランドスーパーコピー

Aluminum Channel Saltwater Resistant

How to shop ugg sale 2024 winter boots Kamik, Kamik, Sandale sport LOBSTER 2, gris foncé rose, filles 'big offers' under $90 great offers

Acid alkali Moth PVC Panel in Guangzhou

China Bearing Analysis

http://www.eibiz.co.th

Customized Size PVC Rod

Neutral Grounding Resistor Cage

Sugar defender Reviews Incorporating Sugar Protector into my everyday

program general health. As somebody who prioritizes healthy consuming, I value the additional defense

this supplement supplies. Since beginning to

take it, I’ve observed a significant renovation in my energy levels and a significant decrease in my need for unhealthy treats such a such

an extensive influence on my every day life. sugar defender

sugar defender Integrating Sugar Protector right into my day-to-day regimen general health.

As a person that prioritizes healthy and balanced eating, I appreciate

the additional defense this supplement supplies.

Considering that beginning to take it, I have actually

seen a marked enhancement in my energy degrees and a substantial decrease in my

wish for harmful treats such a such a profound impact on my daily life.

sugar defender ingredients

Synthetic Fiber Beater Sheet

China Relax Chair Companies

Insulating rubber sheet

Get cheap ugg slippers uk DrMartens, Sandales 4 brides VEGAN BLAIRE, noir, femmes 'daily deals' under $160 discounted products

ブランドスーパーコピー

Nitrile butadiene rubber sheet

Extruder Pvc

Discounted prices ugg style boots DrMartens, Sandale décontractée VOSS, noir, femmes 'amazing products' under $150 limited edition

Best prices for ugg boot sale DrMartens, Botte militaire COMBS, noir, hommes 'shop today' under $110 24/7 support

EPDM rubber sheet

China Chefs Pans and Nonstick Pots and Pans price

Get the lowest price ugg like boots DrMartens, Lacets Logo 140 cm, DR MARTENS 'top-quality deals' under $170 special online sales

mihanovichi.hram.by

Balcony Sofa Set

Oil-resisting rubber sheet

Buy online bailey button uggs DrMartens, Botte Core Pascal Mono,8 oeillets,nr,fem 'best in class' under $70 in stock

Extrusion Pvc Profile

sugar defender official website

Sugarcoating Defender to my daily regimen was one of the very best choices I’ve made

for my health and wellness. I beware concerning what I consume, but this supplement adds an additional layer

of support. I really feel more constant throughout the

day, and my food cravings have reduced substantially. It’s nice to

have something so straightforward that makes such a huge distinction!

CHINA BRONZED FILLED WITH PTFE TUBE

Where to find ugg boots clearance 2024 adidas, adidas, Men's Run 84 Lace Up Sneaker – White Core Black Crystal White 'hot discounts' under $130 special discounts

Buy authentic products ugg boots for sale cheap uk adidas, adidas, Women's Grand Court Alpha 00s Lace Up Sneaker – Wonder White White Wonder White 'seasonal sale' under $50 free gifts

Where to purchase cheap classic ugg boots sale uk adidas, adidas, Men's Kaptir 3.0 Slip On Sneaker – Night Cargo Iron Metallic Silver Pebble 'must have' under $200 exclusive deals

carbon filled ptfe tube

N&F, C&U, SKF, NSK, NTN Bearing MOTOR

matching family stockings

BRONZED FILLED WITH PTFE TUBE

7.5 Kilowatt Motor

ブランドスーパーコピー

fluffy tree skirt

http://www.baronleba.pl

spiral wound gasket outering

China carbon filled ptfe tube

Shop for cheap ugg sale in store adidas, adidas, Women's Grand Court Alpha 00s Lace Up Sneaker – GreyTwo White Silver Metallic 'top rated' under $190 limited offer

Buy cheap online ugg gloves sale 2024 adidas, adidas, Women's VL Court Bold Lace Up Sneaker – Wonder Quartz White White 'new price drop' under $120 holiday sales

fish christmas stocking

clixy.net

Automatic Cutting Saw

Mill Pipe

How to shop ugg boot sale clearance uk Bogs, Bogs, Botte imperméable CLASSIC TALL, noir, femme -LARGE 'special pricing' under $90 online holiday sales

ブランドスーパーコピー

Neoprene Rubber Sheet Rolls

Cold Welded

Where to buy online ugg sale winter 2024 Bogs, Bogs, Botte de pluie GLITTER, or rose, filles 'cheap goods' under $180 best low price

How to purchase cheap ugg sale autumn Bogs, Bogs, Botte de pluie KICKER RAIN CHELSEA, noir blanc, femmes 'super shopping' under $190 fast and cheap shipping

High-strength Neoprene Rubber Sheet

Where to shop ugg australia boots sale Bogs, Bogs, Botte imp. CLASSIC HIGH HANDLES, noir, femmes 'on sale now' under $80 e-commerce sale

Glass Essential Oil Bottle 10ml

Fluorine Rubber Sheet

Amber Bottles For Essential Oils

High Temp Neoprene Rubber Sheet

How to buy smart ugg sale uk 2024 Bogs, Bogs, Botte de pluie RAINBOOT GLITTER, noir, filles 'best online bargains' under $170 quick delivery offers

Neoprene Rubber Sheeting

sugar defender reviews Integrating Sugar Protector right into

my everyday program has been a game-changer for my total

well-being. As a person who already focuses on healthy consuming, this supplement has actually offered an included increase of defense.

in my power levels, and my wish for unhealthy snacks so effortless can have

such a profound influence on my life. sugar defender reviews

sugar defender reviews Discovering Sugar Defender has actually been a game-changer for me,

as I have actually constantly been vigilant about managing my blood

sugar degrees. With this supplement, I feel empowered to

organize my wellness, and my most recent clinical exams have

actually reflected a significant turn-around. Having a credible ally in my corner supplies me with a complacency

and confidence, and I’m deeply grateful for the profound distinction Sugar Defender has

made in my well-being. Sugar defender ingredients

This intervention was unable to find any significant reduction in lipid profile in response to olive oil consumption priligy online

Shop for discounted items ugg boots on sale womens uk Birkenstock, Women's Florida Soft Birko-Flor 3-Strap Sandal – Black 'bargain items' under $60 online sale

Rigid Printed Circuit Board

Buy discounted products ugg genuine leather sale boots Birkenstock, Women's Arizona Birko-Flor 2 Strap Sandal – Black 'free returns offer' under $50 buy direct

Best buy deals ugg boots womens black sale Birkenstock, Women's Mayari Birko-Flor Toe Narrow Sandal – Mocha 'affordable items' under $70 limited offer

PTFE Guide strip

lavidamata.xyz

Online shopping savings ugg boots womens winter sale 2024 Birkenstock, Women's Mayari Birko-Flor Toe Sleeve Sandal – Stone 'amazing sale' under $190 customer favorites

Mobile Phone PCBA

Semi Flex Pcb

PEEK Filled PTFE

ブランドスーパーコピー

Glass Filled Plus Pigment

Graphite Filled PTFE

Through Hole Pcb Assembly

Best buy for ugg sale winter boots uk Birkenstock, Womens Boston Oiled Leather Casual Clog – Black 'limited-time offers' under $180 online bargains

Carbon Filled PTFE

Smt Circuit Board

Luxury Restaurant Chairs

Black Silicone Rubber Sheet

Translucent Silicone Rubber Sheet

http://www.t-formafitness.hu

How to buy discounted ugg classic tall black SoftMoc, Pantoufle à dos ouvert HARLEEN, rose, femmes 'latest trends' under $190 in stock

Best prices for products ugg shopping online SoftMoc, Sandale compensée HARLEY, noir, femmes 'hot deals' under $140 top rated

Thin Silicone Rubber Sheet

Fda-compliant Silicone Rubber Sheet

Best shopping discounts ugg footwear SoftMoc, Pantoufle à dos ouvert HARLEEN, noir, femmes 'best sellers' under $130 trending now

Catering Furniture

Discounted online shopping kids ugg boots clearance SoftMoc, Sandale compensée HARLEY, cognac, femmes 'cheap products' under $160 local stores

Retro Diner Chairs

ブランドスーパーコピー

Textured Silicone Rubber Sheet

Norwood Commercial Furniture

Modern Commercial Outdoor Furniture

Get deals on ugg slipper sale SoftMoc, Sandale compensée HARPER, crème, femmes 'popular products' under $180 same day delivery

Bottom Drawer Slides

How to shop smart ugg boots for girls sale SteveMadden, Richelieu décontracté à lacets JAKKE, gris, hommes 'shop online' under $130 flash sale

Flange Insulation Kit Dimensions

ブランドスーパーコピー

Cheap price deals ugg boots sale low prices SteveMadden, Sandale habillée INVEST, chair, femmes 'hot discounts' under $170 online holiday sales

Discounted online shopping cheap uggs boots sale SteveMadden, Sandale habillée INVEST, blanc, femmes 'new price drop' under $160 e-commerce sale

Undermount Drawer Slides Soft Close

Keyboard Drawer Slides

Flange Insulation Kits Type E

Flange Insulation Kits Type D

ppparagon.co.th

Where to buy affordable ugg mini bailey sale uk SteveMadden, Espadrille JAKKE, noir, hommes 'high quality' under $110 best shopping offers

Cheap online deals ugg shoes sale uk 2024 SteveMadden, Sandale habillée INVEST-R, strass, femmes 'best store deals' under $150 shop fast

Drawer Tracks

Flange Insulation Gasket Kits

Flange Insulation Gasket Kits China

Soft Close Drawer Slides Side Mount

Where to find cheap jimmy choo uggs Birkenstock, Birkenstock, Men's Boston EVA Casual Clog – Black 'shopping spree' under $70 free shipping on all purchases

Silky Thermal Lamination Film

Soft Mica Sheet

Hairline Film

Best online stores ugg boots australia Birkenstock, Birkenstock, Women's Arizona Big Buckle Oiled Leather 2 Strap Narrow Sandal – Cognac 'holiday sale' under $180 exclusive online offers

Best shopping deals ugg kensington boot Birkenstock, Birkenstock, Women's Boston Soft Footbed Suede Clog – Mink 'online discounts' under $140 store promotions

Black Neoprene Rubber Sheet

ブランドスーパーコピー

Thermo Film

http://www.thietbigiainhiet.com

Where to get cheap leather uggs Birkenstock, Birkenstock, Women's Mayari Oiled Leather Toe Sleeve Sandal – Tobacco 'best price today' under $130 best shopping offers

Thermal Lamination Foam

Super Sticky Thermal Lamination Gloss Film

Golden Mica Sheet

Neoprene Rubber Sheet

Find best deals girls ugg boots Birkenstock, Birkenstock, Women's Madrid Big Buckle 1 Strap Narrow Sandal – Cognac 'quality products' under $150 flash sale

Golden Mica Sheet reinforced with Tanged Metal

FLANGE ISOLATING GASKET KITS

HIGH TEMPERATURE SILICONE SHEETS

ブランドスーパーコピー

How to buy smart ugg slippers on sale Puma, Women's Softride Enzo Evo Lace Up Sneaker – Black Pink 'low-cost deals' under $170 best customer service

High Volume Turned Milled Components

Cnc Machining Aerospace Parts

Best offers for ugg snow boots Puma, Men's Softride Enzo Evo Sneaker – White 'get it now' under $140 early bird deals

Foam Cutting

Where to buy online pink uggs Puma, Men's Softride Enzo Evo Lace Up Sneaker – Red Black 'shop for savings' under $180 everyday low prices

Buy now cheap ugg mini Puma, Women's Better Foam Prowl Slip On Sneaker – Black White 'quality bargains' under $160 online shopping

GLASS REINFORCED SILICONE SHEET

Rapid Injection Molding

Sls Rapid Prototyping

How to purchase cheap ugg boots for men Puma, Women's Better Foam Prowl Slip On Sneaker – Black Pink 'must buy deals' under $190 shop with confidence

http://www.dmgs.ru

FKM RUBBER SHEETING

FKM FOOD QUALITY RUBBER SHEETING

Nitrile Rubber Bonded Cork Sheet

Best discounts on ugg boots clearance 2024 SoftMoc, Women's Wensy 01 Vegan Sandal – Red Combi 'fast shipping' under $130 best product deals

Soft Fibration PTFE Sealing Sheet

Care Label

ブランドスーパーコピー

Online cheap shopping ugg slipper sale 2024 SoftMoc, Women's Wedge 01 Vegan Waterproof Boot – Black 'best value' under $150 shop fast

Buy cheap online deals ugg bags Birkenstock, Sandale étroite 2 brides en cuir à grosses boucles ARIZONA BIG BUCKLE, blanc, femmes 'hot items' under $120 limited time offer

10% POB Filled PTFE Tefon Tube

Cotton Tags For Clothing

Tag For Clothes

Shop authentic goods ugg earmuffs Birkenstock, Pantoufle ZERMATT SHEARLING, bleu foncé, hommes 'deal of the week' under $50 best deals online

Neoprene Rubber Superior Sealing Cork Rubber Sheet

http://www.borisevo.ru

Anti-static Rubber Sheet Pad

Clothes Tag Make

Eco Friendly Clothing Tags

Online cheap shopping ugg kensington Birkenstock, Sandales étroites YAO, blanc, femmes 'best in class' under $150 top picks

Mica Tube

Mica Tape

Medical Bedside Table

Best prices for ugg classic mini boots sale uk Clarks, Women's Suttyn May Casual Wide Loafer – Black 'budget-friendly shopping' under $110 quick processing

Overbed Table With Vanity

ブランドスーパーコピー

Affordable shopping ugg wool slippers sale Clarks, Women's Zylah May Platform Loafer – Black Crinkle Patent 'today’s hot sale' under $80 premium products

Mica Paper

Best prices online ugg australia leather boots sale Clarks, Women's Ellanie Hope Wide Dress Heel – Black Suede 'top product picks' under $90 buy today

Where to get cheap ugg winter boots sale clearance Clarks, Women's Daiss30 Trim Loafer – Dark Tan 'cheap goods' under $130 free shipping worldwide

Mica Roll

Adjustable Bedside Table

Hill Rom Patient Mate Overbed Table

Ikea Over Bed Table Malm

Find cheap deals ugg boots with faux fur Clarks, Women's Zylah May Platform Loafer – Black 'big markdowns' under $100 best discount deals

Mica Plate

http://www.sunflavour.co.jp

Hi there I am so grateful I found your blog page, I really found you by error, while I was looking on Aol for

something else, Anyhow I am here now and would just like to say thanks a

lot for a incredible post and a all round exciting blog (I also love the theme/design), I don’t have time

to read it all at the moment but I have bookmarked it and also added in your

RSS feeds, so when I have time I will be back to read more, Please do keep up

the superb jo.

Best online shopping deals uggs Converse, Men's Chuck 70 Hi Top Sneaker – Green Envy Egret Black 'best sellers' under $190 popular deals

RING JOINT GASKET

ブランドスーパーコピー

RUBBER GASKETS

http://www.transhol.pl

Extrusion De Aluminio

Find best products ugg australia Converse, Infant's Chuck Taylor All Star V2 Transformers Canvas Sneaker – Black Yellow Red 'free returns' under $160 great deals online

Aluminium Extrusion Heat Sink

O-RINGS

CERAMIC FIBER GASKETS

Extruded Aluminum Rollers

Aluminium Heat Sink Extrusion

Online cheap shopping ugg slippers Converse, Women's Chuck Taylor All Star Hi Top Sneaker – Viper Violets 'best discounts' under $150 best online offers

Buy authentic items cheap ugg boots uk Converse, Women's Chuck Taylor All Star Cruise Platform Sneaker – Mud Mask Egret White 'best offer' under $170 unbeatable prices

Where to find authentic ugg sale Converse, Men's Chuck Taylor All Star Optimus Prime Hi Top Sneaker – Black Fever Dream White 'special deals' under $140 fast and convenient

NON-METALLIC GASKETS

Hollow Extrusion Die

Colored Pencil Case

Online cheap deals ugg bailey button classic short sale UGG, Botte CLASSIC CARDI CABLED KNIT, gris, femmes 'best online bargains' under $90 big deals

Large Pencil Bag

ブランドスーパーコピー

How to find discounts ugg black friday 2024 boots Clarks, Women's Breeze Emily Slip On Casual Shoe – Olive 'exclusive products' under $90 featured products

Synthetic Fiber Rubber Gasket

Cheap shopping options ugg boots chestnut sale Clarks, Women's Kyndall Faye Dress Heel – Black 'best quality items' under $80 hot deals

Asbestos Beater Sheet

Pencil Case Bag

Best prices for authentic ugg winter sale UGG, Botte CLASSIC CARDI CABLED KNIT, noir, femmes 'cheap goods' under $100 hot sale

Distributor

Affordable online shopping ugg boots sale for women Clarks, Women's Camzin Pace Casual Shoe – Black 'low prices' under $70 top picks

Promotional

Styrene-butadiene rubber sheet

Acid Resistant Mineral Fiber Rubber Sheet

http://www.kmu.ac.th

Oil Resistant asbestos Sheet

L3 Ethernet Switch

8 Port Switches

Best deals on cheap products ugg australia bailey button UGG, Botte à lacets YOSE PUFFER LACE, noir, femmes 'popular products' under $60 unbeatable online prices

Where to buy authentic chestnut ugg boots DrMartens, Lacets Logo 140 cm, DR MARTENS 'online store' under $60 holiday product sale

12 Port Ethernet Switch

Internet Access Point

quawas.jo

Anti-Rot Rubber Tape

Buy products at low cost buy uggs UGG, Botte à plateforme BRISBANE CHELSEA, noir, femmes 'best value online' under $50 trending online sales

Discounted prices ugg kids DrMartens, Lacets jaune 140 cm, DR MARTENS 'discount online' under $150 exclusive shopping deals

Oil Resistant Mineral Fiber Rubber Sheet

Rubber Sheet Reinforce With Cloth

Home Network Switch

Get cheap ugg clearance DrMartens, Lacets arc en ciel 140 cm, DR MARTENS 'free returns offer' under $160 online store deals

Rubber Sheet

ブランドスーパーコピー

Rubber Seal Strip